Let's cut through the noise. U.S. Treasury bond rates aren't just numbers on a financial website; they're the bedrock of the global financial system, a crystal ball for the economy, and a critical tool for anyone with a savings account, a 401(k), or a mortgage. If you've ever wondered why your bond fund lost value when news about the Federal Reserve came out, or felt confused about whether to lock in a long-term rate or stay short, you're in the right place. This isn't about memorizing definitions. It's about understanding the forces at play so you can make informed decisions with your money.

What You'll Learn in This Guide

What Treasury Bond Rates Really Tell You (It's Not Just Interest)

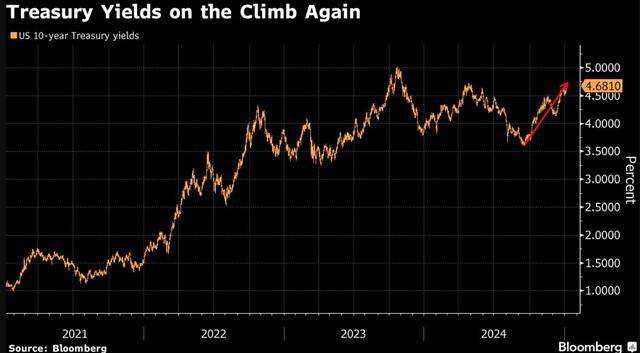

When you see a rate like "2-Year Treasury at 4.75%," that's the yield. It represents the annual return an investor would receive if they bought that bond at its current price and held it to maturity. But here's the crucial part everyone misses: that yield is a composite signal. It's not set by the government in a vacuum. It's determined by a daily auction where big institutions bid, and it reflects three things mashed together: expectations for future Federal Reserve policy, the market's demand for safe haven assets, and predictions for long-term inflation.

Think of it this way. A 10-year Treasury yield of 4.2% isn't just "4.2% interest." The market is essentially saying, "We think the average of where short-term rates will be over the next decade, plus a little extra for the risk of inflation and holding a long-term bond, equals 4.2%." It's a forecast, not a decree.

The Four Key Drivers Moving Treasury Rates

Rates don't move randomly. They react to specific inputs. Ignoring any one of these is like trying to forecast weather without considering air pressure.

1. Federal Reserve Policy (The Short-Term Captain)

The Fed controls the federal funds rate, which is the overnight borrowing rate for banks. This is the anchor for the short end of the Treasury yield curve (think 1-month to 2-year bonds). When the Fed hikes rates to fight inflation, yields on short-term Treasuries shoot up almost immediately. Their meeting minutes, dot plots, and even speeches by chairs like Jerome Powell are dissected for clues. The market isn't just reacting to what the Fed did; it's reacting to what it thinks the Fed will do next.

2. Inflation Expectations (The Long-Term Shadow)

For longer-term bonds (5 to 30 years), inflation is public enemy number one. Why? Because inflation erodes the fixed payments a bond promises. If investors think inflation will average 3% over the next 30 years, they'll demand a yield significantly higher than 3% to compensate for that loss of purchasing power. Data like the Consumer Price Index (CPI) and the Fed's preferred PCE index are major catalysts. Sometimes, long-term yields move more on an inflation scare than on an actual Fed action.

3. Economic Growth Outlook

Strong economic data (high GDP growth, low unemployment) can push rates up for two reasons. First, it suggests stronger demand for capital, which competes with bonds. Second, it raises the risk that a hot economy will fuel inflation, prompting the Fed to be more aggressive. Conversely, weak data or fears of a recession send investors fleeing to the safety of Treasuries, driving prices up and yields down.

4. Global Demand and Geopolitical Stress

U.S. Treasuries are the world's ultimate panic room. When a war breaks out, a banking crisis hits Europe, or global growth fears spike, money pours into Treasuries from around the globe. This surge in demand pushes yields lower, sometimes even overriding what domestic economic data would suggest. Central banks (like Japan's or China's) are also massive holders, and their buying or selling programs can influence the market.

Decoding the Yield Curve: The Market's Mood Ring

The Treasury yield curve is a line plotting the yields of bonds with different maturities, from one month to 30 years. Its shape is a powerful storybook.

| Curve Shape | What It Looks Like | What It Typically Signals | Investor Implication |

|---|---|---|---|

| Normal (Upward Sloping) | Short-term rates lower than long-term rates. | A healthy, growing economy. Investors expect higher rates/inflation in the future and demand more yield to lock money up long-term. | Rewards for taking duration risk. "Rolling down the curve" strategies can work. |

| Flat | Little difference between short and long yields. | Uncertainty. The market thinks the economic cycle is late, and future growth/inflation may stall. Often a transition phase. | Little extra reward for going long. Focus on credit quality or other sources of return. |

| Inverted (Downward Sloping) | Short-term rates higher than long-term rates. | Expectation of economic slowdown or recession. The market believes the Fed will be forced to cut rates in the future to stimulate a weak economy. | A warning sign. Cash and short-term instruments may outperform. Long-term bonds could rally if recession hits. |

| Steepening | The curve is getting steeper (long rates rising faster than short rates, or short rates falling faster). | Often signals expectations of stronger future growth and inflation after a period of fear or policy easing. | Can benefit banks. Long-term bonds may face price pressure as yields rise. |

I've seen investors panic when the curve inverts, dumping all their bonds. That's often a mistake. An inversion is a forecast, not an immediate command. In fact, once a recession materializes and the Fed starts cutting, long-term bonds (whose yields peaked before the cuts) often see the biggest price rallies. The curve holds clues for timing.

Practical Investment Strategies for Any Rate Environment

You don't need a Ph.D. to act on this. Here are concrete approaches, not theoretical fluff.

When You Expect Rates to Rise (A Hawkish Fed, Hot Inflation)

- Shorten Duration: This is your primary defense. Move money into shorter-term Treasuries (under 2 years), T-bills, or floating-rate notes. Your money isn't locked up at a low rate, and you can reinvest at higher yields soon.

- Consider a Ladder: Build a bond ladder with rungs every 6-12 months. As each rung matures, you reinvest the principal at the new, presumably higher, prevailing rate. It's a disciplined way to avoid trying to time the peak.

- What to avoid: Loading up on long-duration bond funds or zero-coupon bonds. They get hit hardest when yields climb.

When You Expect Rates to Fall (Recession Fears, Fed Pivoting)

- Extend Duration Selectively: Locking in a longer-term yield before the Fed cuts can be profitable. If you buy a 10-year bond at 4.5% and the market yield drops to 3%, the price of your bond rises.

- Look at the Long End: Longer-term bonds (20-30 year) have more price sensitivity (duration), so they amplify gains in a rally. This is for the more aggressive part of a portfolio.

- A Personal Tactic: In late 2023, when the yield curve was deeply inverted and everyone was screaming "recession," I started slowly adding to intermediate-term Treasury ETFs (like IEF) instead of crowding into the short end. The idea was to capture some of the eventual rally when the pivot came, without going all-in on the volatile long end. It required patience.

The All-Weather, Set-and-Forget Approach

For core portfolio diversification, a simple barbell strategy works wonders. Allocate a portion to short-term Treasuries for stability and liquidity. Allocate another portion to a broad intermediate-term bond fund for income. This balances interest rate risk. Rebalance annually. It's boring, but it prevents you from making big, emotional bets on the direction of rates, which even professionals get wrong.

Common Investor Mistakes to Avoid (The Unspoken Pitfalls)

After watching markets for years, the same errors pop up.

Mistake 1: Chasing Yield Blindly. "This corporate bond fund yields 6%, but the Treasury fund only yields 4.5%!" That extra 1.5% is credit risk, not free money. In a downturn, those corporate bonds can get hammered while Treasuries rally. Compare yields within the same asset class. A high-yield savings account paying 5% is often a smarter, safer alternative to stretching for yield in a risky bond.

Mistake 2: Treating "Rates" as a Monolith. Saying "rates are going up" is too vague. Are short-term rates going up on Fed action while long-term rates fall on recession fears (a flattening or inverting curve)? Your strategy changes completely based on which part of the curve is moving. Always look at the shape.

Mistake 3: Ignoring Taxes. Treasury interest is exempt from state and local income taxes. For someone in a high-tax state like California or New York, a 4% Treasury yield might be equivalent to a 4.5% or 5% taxable corporate bond yield after taxes. Do the math for your situation. The TreasuryDirect.gov website lets you buy bonds directly, tax-free at the state level.

Mistake 4: Thinking a Bond Fund is Just Like a Bond. If you buy a 10-year bond and hold it, you get your principal back at maturity regardless of price swings. If you buy a 10-year bond fund, it never matures. It constantly rolls its holdings. In a sustained rising rate environment, the fund's price can keep drifting lower. Know what you own: individual bonds for known maturity/cash flow, funds for diversification and trading.

Comment desk

Leave a comment